Strip away the price chart, the discourse, and the ETF flows. What's left is Ethereum's on-chain economy — the gas paid by every smart-contract execution, every stablecoin transfer, every rollup batch that settles back to the base layer. That's the thing your ETH gives you a per-token piece of, and it's measurable by the block.

After 2024's Dencun upgrade moved rollup batches onto a separate blob market, the L1 gas everyone watches got smaller — and the per-token fee surface with it. The network underneath kept being used; the fee surface didn't keep pace. The question of where ETH stands today is what that picture — heavy usage, compressed on-chain economy — actually means for the asset.

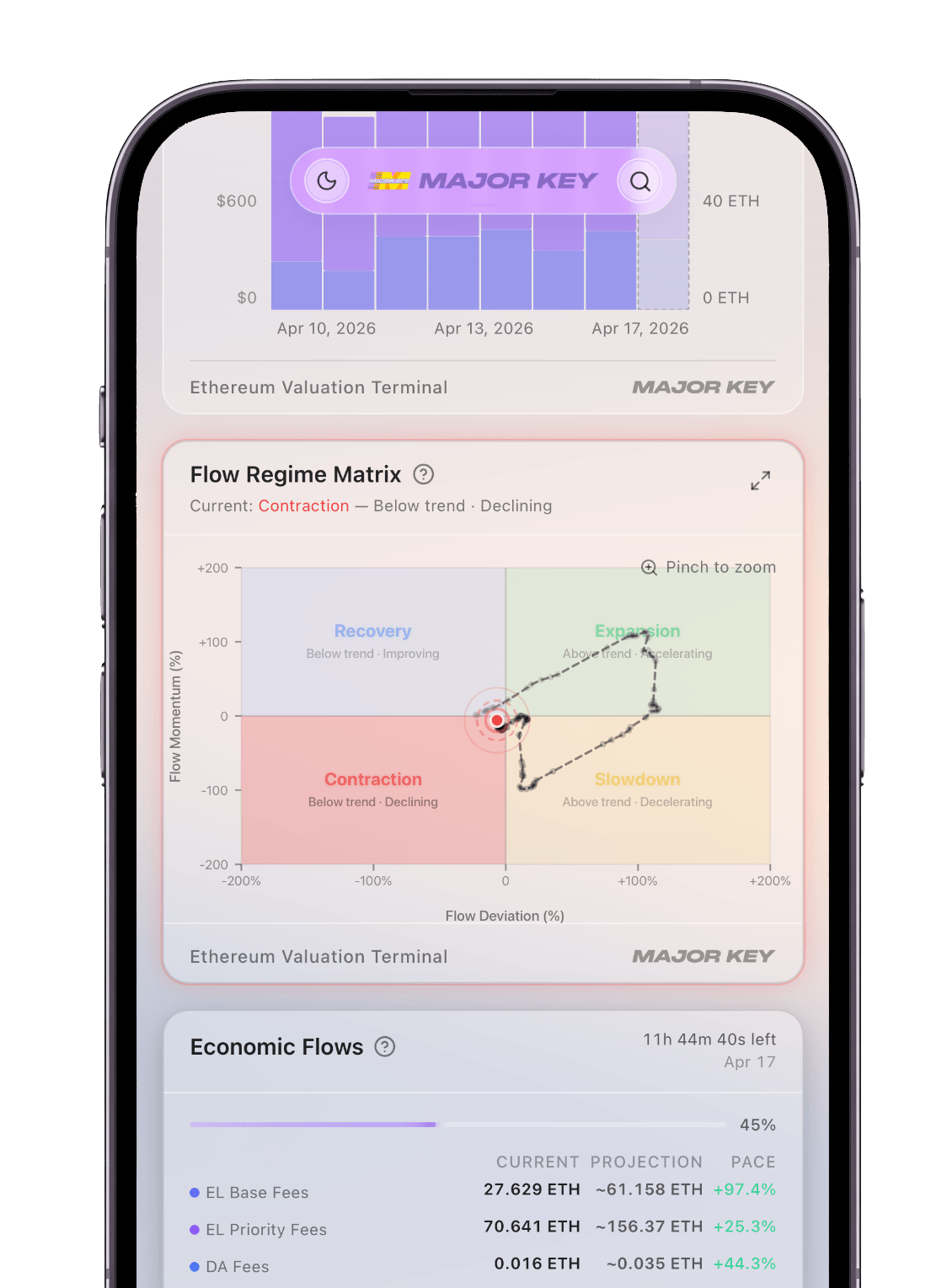

Below is what that looks like as of July 5, 2026 — the underlying activity of the Ethereum network over the last six months, a few simple readings of what the network is doing right now, and where the per-token supply is moving.